-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

LONGi Green Energy Technology (601012.CN) - With significant technical advantages, the leading position is robust

Thursday, September 1, 2022  2655

2655

LONGi Green Energy Technology(601012)

| Recommendation | Buy |

| Price on Recommendation Date | $52.800 |

| Target Price | $67.940 |

Weekly Special - 603605.CH Proya Cosmetics

Brief introduction to the company

LONGi Green Energy(601012.CH) is a world-leading monocrystalline silicon wafer and vertically integrated solar module company. Its main business includes R&D, production, and sales of monocrystalline silicon ingots, monocrystalline silicon wafers, and solar modules. At the present, the company has formed a complete supply chain for the development, construction, and operation of mono-silicon rods, silicon wafers, monocrystalline silicon rods, silicon wafers, monocrystalline cells, modules, and PV power plants. It is also the world's largest manufacturer of monocrystalline silicon wafers and modules.

A review of H1 2022 Results

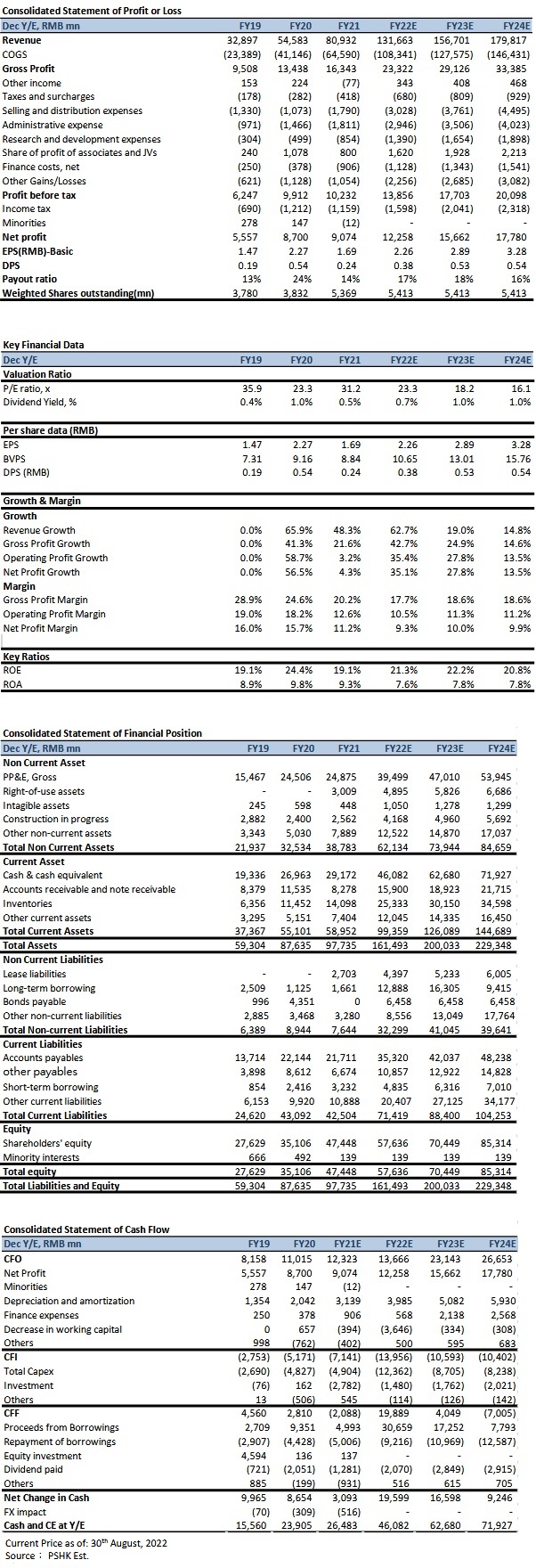

The company has announced the operating data from January to June 2022. The company achieved an operating income of ¥50.4 bn, up 43.6% YoY, with revenue in Q2 being ¥31.8bn, up 65.4% YoY, and up 71.1% QoQ; the net profit attributable to shareholders was ¥6.48 bn, up 29.8% YoY, with net profit in Q2 being ¥3.82 bn, up 53.2% YoY, and up 43.3% QoQ. The results indicate that although the company was affected by high material prices and rising shipping costs, the company's module shipments rose significantly in Q2, which accelerated the company's revenue growth and net profit began to rise.

With obvious advantages in brand and distribution channels, market share is expected to increase

We believe that the company has strong advantages in brand and distribution channels. A solar module business is a To B and To C business, hence there are high requirements of the brand, reliability, and distributing channels for a solar module company to succeed. In terms of the brand advantage, the modules produced by the company are of high quality and high reliability, and the reliability of the products has been recognized by customers. The US Renewable Energy Testing Center(RETC) and an independent third-party testing laboratory PVEL respectively selected LONGi as a High Achiever and the global Top Performer in the solar module industry, certifying the reliability of its modules and the brand of LONGi. In terms of distribution channels, the company has extensive global distribution channels. The company has manufacturing facilities and sales offices in more than 150 countries and regions worldwide. The company has set up production and manufacturing facilities in China, Vietnam, and Malaysia, as well as sales offices in the United States, Japan, India, Australia, the United Arab Emirates, and other countries. Due to the company's strong distribution channels, the company's overseas module revenue in 2021 increased by 81% YoY, much higher than the domestic growth rate of 37%, and the overseas module business accounted for 62% of total revenue. Because the company has such obvious advantages, the management of the company has expressed clear market share targets. In 2 years, LONGi expects the market share of the silicon wafer business to be 45%-50%, and the market share of the module business will increase to the current 25%-30%, up from about 23% in 2021.

The company has invented frontier solar cell technologies

The company has in-depth research on TOPCon, HJT, and HPBC batteries. First, the photoelectric conversion efficiency of the company's TOPCon and HJT cells continues to set new industry records. In July 2021, the conversion efficiency of the monocrystalline P-type TOPCon cell developed by LONGi's R&D team reached 25.19%, surpassing the world record (25.02%) set by the company, and was confirmed by the world-recognized Germany's Institute for Solar Energy Research Hamelin. In June 2022, the company broke the world record for the fourth time in one year, announcing that the conversion efficiency of HJT cells has increased to 26.50%, which is 1.24% higher than that announced on 3rd June 2021. Second, the company's HPBC cell(One of the IBC cells) leads the industry. IBC is the most difficult cell technology in manufacturing crystalline silicon cells, and the use of P-type silicon wafers further increases the difficulty of manufacturing an IBC cell. According to an environmental impact assessment of the LONGi 4GW Taizhou monocrystalline cell project, the company has not only mastered the IBC process, but also made use of P-type silicon wafers in manufacturing HPBC cells. Third, the company has mastered the N-type silicon wafer process, which requires high purity. On the contrary, second-tier manufacturers need to spend time learning how to reduce the cost of N-type silicon wafers with low impurity. We believe that regardless of whether the mainstream technology in the future will be HJT, TOPCon, or IBC, the company now has enough technical reserves to adapt to any of these new cell technologies.

The company has entered BIPV and hydrogen production market, bringing the possibility of a second growth curve for the company

The company has already entered BIPV and hydrogen production markets. In terms of BIPV business, the company released the first BIPV product, LongDing, in August 2020, and later acquired part of the shares of metal roof construction company Center International Group Co. Ltd in 2021, with a shareholding ratio of 24.74%. The two parties will combine their respective advantages to jointly promote cooperation in BIPV product research and development, market development, and related fields, entering the big market of distributed photovoltaics and BIPV. In terms of the hydrogen production business, the company has a production capacity of 500MW alkaline water electrolyzers, and the production capacity will reach 5-10GW in the next five years. The electrolyzer is designed with a high current density and a hydrogen production capacity above 1000Nm³/h. The company's first alkaline water electrolyzer was manufactured in October 2021. In addition, on April 12, 2022, three 1000Nm3/h electrolyzers were successfully shipped. We believe that BIPV and hydrogen production market will become the company's second growth curve in the future, which could boost the company's valuation.

Company valuation

We believe that the company is the leader in the solar module industry, with advantages in brand, distribution channel, and cell technologies. It is expected that the company's module business market share will increase. In addition, the company's entry into the BIPV and hydrogen production markets could boost the company's valuation. We estimated that the company's EPS in 22/23 will be ¥2.26/2.89 respectively, corresponding to a P/E of 23.3/18.2x in 22/23. By considering the average P/E of peers, we have conservatively given the company a P/E of 35x in 2022, corresponding to the target price of ¥67.94, and a "buy" rating. (Current price as of 30th August).

Risk factors

(1)Industry competition intensifies. (2) Policy changes. (3) New solar cell technologies replacement. (4)Raw material prices rise. (5) Product prices fall.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()